Big headlines or “new economic models” might have your attention with a highly likely % for an economic recession. Yet, despite whispers of an inevitable recession, a closer look at the data tells a different story. While uncertainty and challenges do exist, the US economy continues to hold surprisingly strong. Unemployment figures remain low, consumers are still opening their wallets, and industries are adapting rather than crumbling.

Could it be that whispers of recession are exaggerated? Could the economy defy expectations and achieve what analysts deem unlikely – a soft landing? Let’s dive into the numbers and explore why the US economy might just pull off a surprising feat of resilience.

Predicting recessions is notoriously difficult, even with complex models considering inflation, bond yield, CPI, and more. For this analysis, we’ll zero in on three key metrics that often offer early signs of an economic slowdown: the unemployment rate, the S&P 500 index, and the direction of interest rate changes.

Unemployment Rate

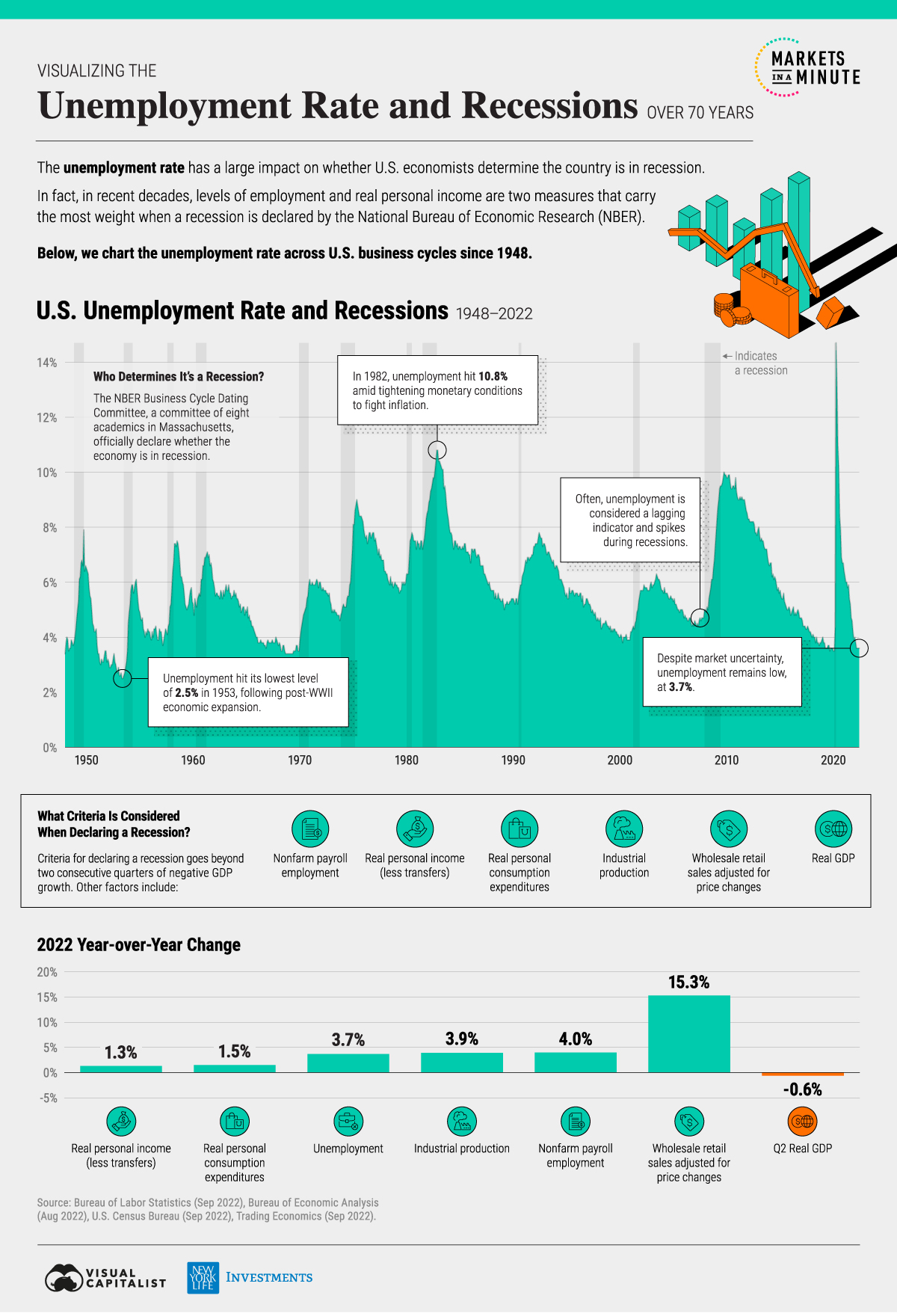

History provides a stark lesson: Recessions are almost always accompanied by sharp increases in unemployment. As businesses falter, they’re forced to shed workers, leaving millions without paychecks. Currently, the US unemployment rate remains near historic lows at 3.70%. In the late 1970s, the US was grappling with runaway inflation. To combat this the Feds dramatically increased the interest rates. Result, borrowing got expensive, in 1972 unemployment rate was around 5.8% and by 1982, it skyrocketed to 10.8% as per the graph below. The US actually experienced a brief recession starting in 1980 as well, making the early 80s a brutal economic period. Even after the Fed shifted course on interest rates, the jobs market was slow to bounce back, showing the lingering effects of an unemployment shock.

A strong job market matters as steady paychecks promises more cash flow through the economy. Additionally, Low unemployment reduces the need for government support programs like unemployment benefits. This can potentially ease budgetary pressures and create a more stable fiscal environment. Professional forecasters expect the unemployment ratio average around 3.9%, making a decline from the previous estimate of 4.1%.

While the overall unemployment rate is positive, Low unemployment alone cannot promise will avoid a recession. Inflation, geopolitical shocks, and drastic shifts in Federal Reserve policy can still create problems. So unemployment rate if not the only metric, but is considered a strong metric on determining the position of recession in a country.

Stock Market: S&P 500

As of the drafting of this blog, the top 7 companies, (Apple, Microsoft, Amazon, etc.) comprise an outstanding 28% of the index’s weight. The S&P 500 no longer truly reflects the health of 500 diverse companies. It’s heavily influenced by the performance of a handful of players within specific sectors.

Exhibit 23 shows the indexed return of 70% by the magnificent 7 and 6% by the S&P 493 companies. Remove the 7 out of the equation, the S&P 500 is down. Forget what Wall Street talking heads tell you. The stock market isn’t a foolproof oracle of the economy’s health. With immense power concentrated in the hands of a few mega-companies, the S&P 500 can both hide gathering storm clouds and create false alarms about an impending recession. If these companies continue to rake in profits even amidst slowing sales, it tells a story about who bears the brunt of economic hiccups (hint: not their CEOs). This may signal growing income inequality, which itself contributes to recession vulnerability.

UnFiltered Truth: Markets don’t equal the economy –

- The S&P 500 remains an important metric, but blindly worshipping it is dangerous. Investors and everyday citizens need to look beyond the headlines for data about smaller businesses, wage growth, and diverse industry health.

- An isolated shock to these top companies, or a change in investor sentiment towards just the tech sector, can send shockwaves through the entire market, sparking panic out of proportion to the real economic threat.

This concentration is about far more than just stock prices; it’s about corporate influence over entire supply chains and potentially even policymaking. Recessions don’t hit everyone equally. Exposing how wealth concentrated is in a few companies leaves the ‘little guy’ more vulnerable in the end.

Interest Rates

Interest rates for years have been a major tool used by the feds to either stoke recessions or try to desperately avoid them. Understanding the Federal Reserve’s power is key to seeing how much of your economic fate is, quite frankly, out of your hands. They don’t set ALL rates, but their actions on short-term borrowing sets off a chain reaction across the financial system.

Economically speaking, Interest rates does work to bring costs down. As raising rates makes borrowing more expensive. This theoretically cools down excessive spending and slows runaway inflation. But like with harsh medicine, if the dosage is wrong, it backfires. Hikes punish people already struggling with credit card debt, drive some businesses to the brink, and make buying a home near impossible for everyday folks. It’s not neat, clean surgery; more like economic amputation.

Go look at any major recession… you’ll likely find aggressive interest rate hikes preceding the misery. Correlation doesn’t equal causation always, but this pattern demands scrutiny.

A hypocrisy to look for –

- Rate hikes often come with promises of ‘bringing things back to normal’. For big corporations sitting on cash piles, sure. For those living paycheck to paycheck? ‘Normal’ might turn rapidly into financial ruin.

- Watch if hikes hurt everyday borrowers, but banks somehow find loopholes to NOT make your savings account suddenly earn significantly more interest. The system knows who it serves best.

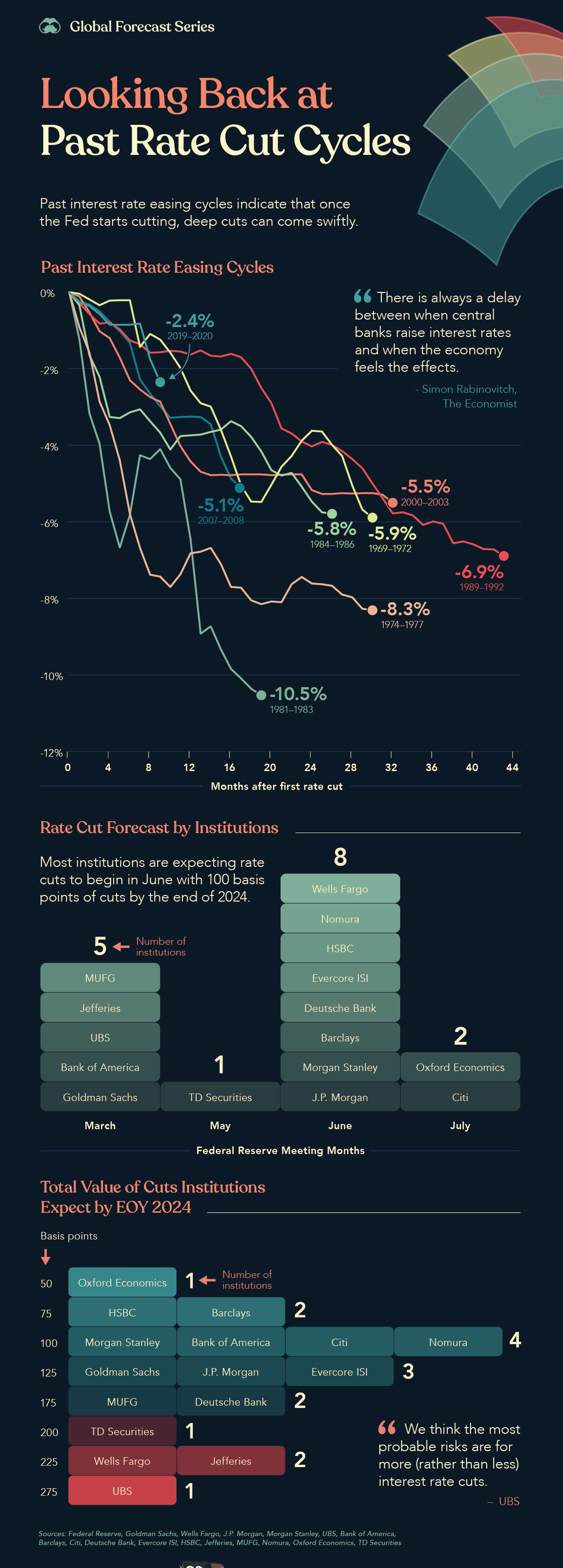

- From the survey below, major institutions including Morgan Stanley, Citi, Bank of America, etc. forecasts a rate cut of 100 basis point somewhere around in June this year. How would that look for the rest of 2024, let’s analyze.

Rate Cuts (100 basis points) –

- Cheaper borrowing in theory stimulates spending. Businesses invest in expansion, hiring might tick up, stuck projects (like home building) get back up.

- With cheaper borrowing, investors may pour money back into stocks, creating a rally… especially in beaten-down stocks of the S&P 500.

In the End, Economics textbooks like neat answers. Real life is messier. Expect to see experts contradict each other after such a cut. This move highlights that a good deal of our fate rests on factors beyond our individual control.

Importantly to add never underestimate the pressure to ‘save’ an economy ahead of a major election. A short-term sugar high from cuts might hide long-term poison pills.

Bonus : UnFiltered Questions

- Does a market rise reflect real economic hope, or just speculators gambling on easy money from the Fed?

- Is our spending problem due to interest rates being TOO HIGH, or something else entirely (broken supply chains, income inequality, corporate greed jacking up prices even if not a supply issue)?

Leave a Reply