Buy Now, Pay Later (BNPL) services have exploded in popularity in recent years, offering consumers a seemingly convenient way to finance purchases without traditional credit cards. But are BNPL services really a better deal than credit cards? Let’s delve into the pros and cons of each option to help you decide which is right for you.

What is BNPL?

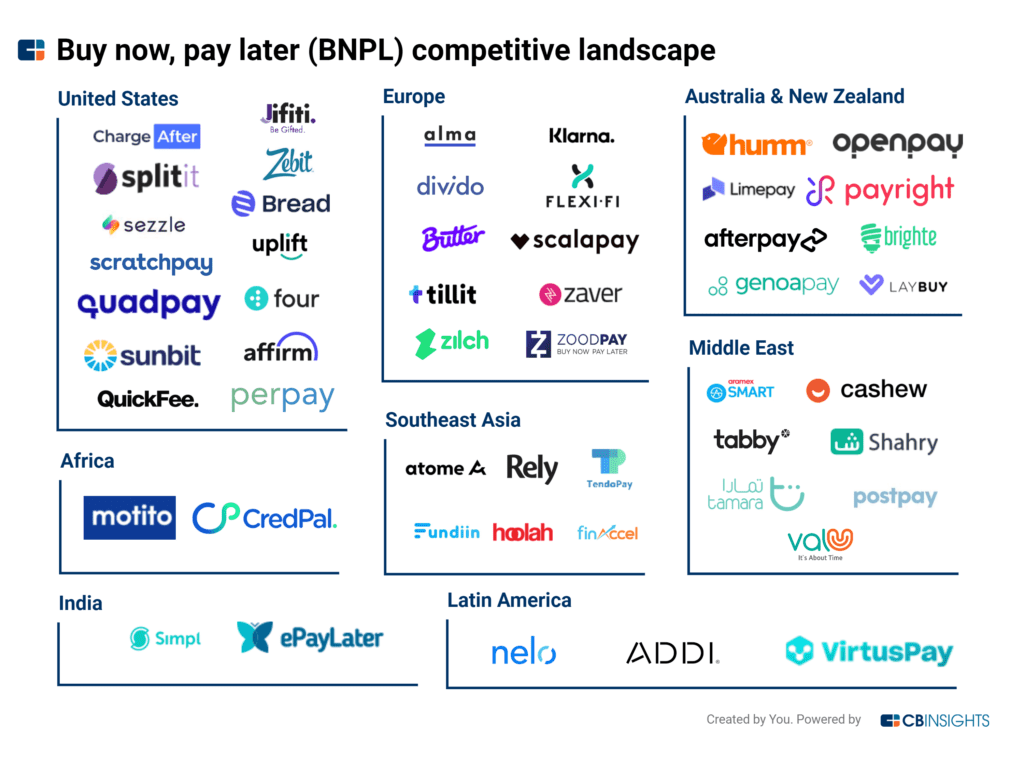

BNPL services allow you to split the cost of a purchase into smaller installments, often interest-free, over a short period. Popular BNPL providers include Apple Pay, Klarna, Affirm, Afterpay, and Sezzle. These services typically partner with retailers, allowing you to use BNPL at checkout for online and in-store purchases.

The Appeal of BNPL

- No upfront cost: You don’t need to pay the full amount of your purchase upfront, making it easier to manage your budget.

- Interest-free (sometimes): Many BNPL plans offer interest-free financing if you pay off your balance within a set period, typically 6-12 weeks.

- Fast and easy approval: BNPL providers often have less stringent approval requirements than credit cards, making them easier to qualify for.

- No credit check: Some BNPL providers don’t perform credit checks, which can be helpful for those rebuilding their credit or with limited credit history.

The Downsides of BNPL

- Hidden fees: Some BNPL plans charge late fees, processing fees, or other hidden charges that can add up quickly.

- Temptation to overspend: The ease of using BNPL can lead to impulse purchases and overspending, especially if you’re not careful about budgeting. An Experian survey found that 31% of BNPL users admitted to making purchases they otherwise wouldn’t have been able to afford.

- Debt trap: If you miss payments or can’t pay off your balance within the promotional period, you could be hit with high interest rates and fees, leading to a debt trap. The same Experian survey stated around 23% of BNPL customers have regretted financing this way.

- Limited purchase protection: Unlike credit cards, BNPL services typically offer limited purchase protection and fraud liability.

- Not reported to credit bureaus: Using BNPL responsibly won’t help you build your credit score, as payments are not reported to credit bureaus.

Credit Cards: A Traditional Option

Credit cards have been around for decades and offer a familiar way to make purchases and manage finances.

The Advantages of Credit Cards

- Wider acceptance: Credit cards are generally accepted at a wider range of merchants than BNPL services.

- Rewards programs: Many credit cards offer rewards programs that allow you to earn cash back, travel points, or other perks on your spending.

- Purchase protection: Most credit cards offer purchase protection and fraud liability, which can help you recoup losses if your card is lost, stolen, or used fraudulently.

- Credit building: Responsible credit card use can help you build your credit score over time. A recent survey by LendingTree found that 60% of people were able to improve their credit scores by actively using and managing credit cards responsibly.

The Drawbacks of Credit Cards

- Interest charges: If you don’t pay your credit card balance in full each month, you’ll be charged interest, which can be high.

- Annual fees: Some credit cards have annual fees, which can add to the cost of using the card.

- Temptation to overspend: Similar to BNPL, credit cards can also tempt you to overspend if you’re not disciplined with your finances. A survey from CreditCards.com revealed that 50% of credit card holders admit to sometimes carrying a balance and falling into credit card debt.

So, Which is Right for You?

The decision of whether to use BNPL or a credit card depends on your individual financial situation and spending habits. If you’re a disciplined spender who can pay off your balance in full each month, a credit card could be a good option to earn rewards and build your credit. However, if you’re prone to impulse purchases or have trouble managing debt, BNPL might be a better choice, as long as you’re aware of the fees and potential risks.

“He who is quick to borrow is slow to pay”

– Thomas Tusser

Here are some additional tips to keep in mind:

- Do your research: Before using any BNPL service or credit card, be sure to read the terms and conditions carefully to understand the fees, interest rates, and other charges.

- Budget carefully: Only use BNPL or credit cards for purchases you can afford to repay. Create a budget and stick to it to avoid overspending.

- Pay off your balance in full: If you use a credit card, aim to pay off your balance in full each month to avoid interest charges.

- Use BNPL sparingly: If you choose to use BNPL, use it sparingly and only for small purchases.

- Monitor your credit: If a BNPL provider performs a hard credit check on your account, it could temporarily lower your credit score. Additionally, late or missed payments may be reported to credit bureaus, further affecting your score.

Leave a Reply